Climate mandates under ISSB: A template for investors

Hello everyone,

In my previous newsletter on climate scenario analysis, many readers were unaware of the new ISSB climate reporting mandates, how imminent they are in some countries and what to do. So in this weeks newsletter, I thought it would be helpful to share some expected timeframes, offer first steps to prepare and also provide a comprehensive template for investors.

What is the ISSB and why is it a big deal?

In June 2023, the International Sustainability Standards Board (ISSB) published a landmark climate standard known as the IFRS S2 Climate-related Disclosures. The ISSB is part of the International Financial Reporting Standards (IFRS) foundation, which is the global body that develops accounting standards that most major jurisdictions adopt as part of their accounting standards. The objective of IFRS S2 is to mandate companies into revealing information about their climate risks and opportunities.

For the first time reporting entities will have a legal obligation to report their climate information to the same level of quality as other financial information in their general purpose financial reports.

Who is impacted and when?

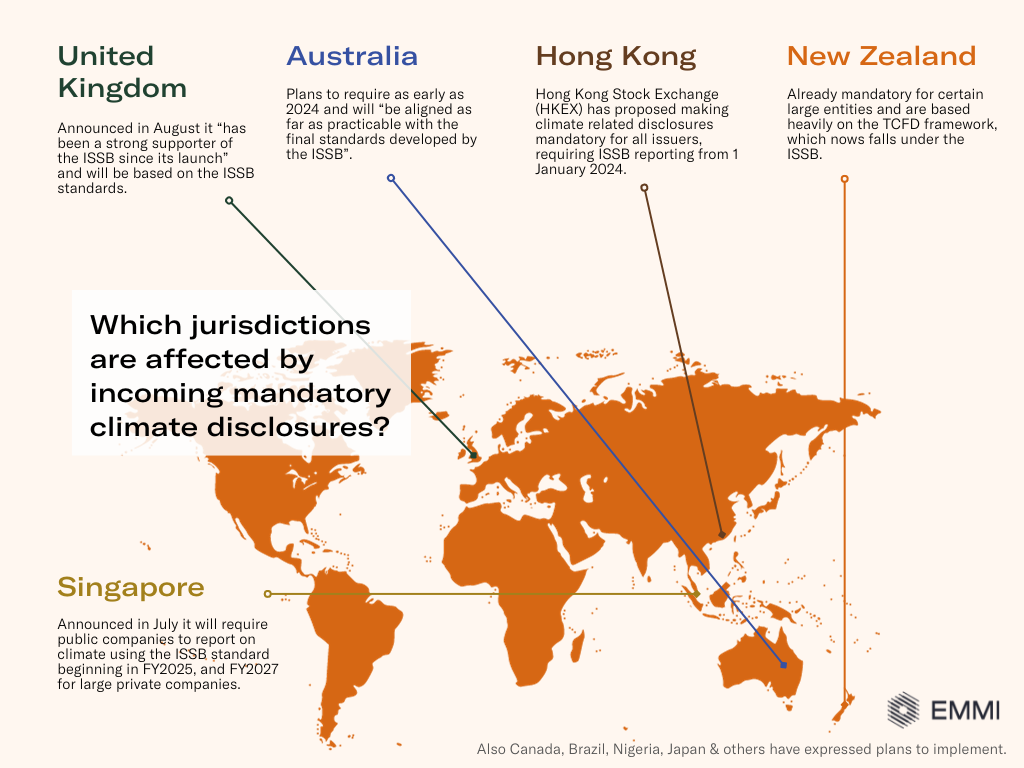

Australia: The Australian government plans to require businesses and financial institutions to report their climate-related financial information as early as 2024 and will “be aligned as far as practicable with the final standards developed by the ISSB”.

New Zealand: Climate reporting is already mandatory in New Zealand for certain large entities and are based heavily on the Task Force on Climate-related Financial Disclosures (TCFD) framework, which nows falls under the ISSB.

Singapore: The government announced in July it will require public companies to report on climate using the ISSB standard beginning in FY2025, and FY2027 for large private companies.

United Kingdom: The government announced on 2 August 2023 it “has been a strong supporter of the ISSB since its launch” and will be based on the ISSB standards.

Hong Kong: Hong Kong Stock Exchange (HKEX) has proposed making climate related disclosures mandatory for all issuers, requiring ISSB reporting from 1 January 2024

.

First steps to prepare for ISSB

1. Are you a reporting entity?

In general large, listed and financial institutions are the entities required to report under ISSB, but those definitions vary for each country. Singapore for example, is mandating even large private companies by 2027.

2. Get your climate data pipeline ready

Under ISSB, entities must report their climate-related financial disclosures alongside their financial statements for the same reporting period.

This is challenging since typically climate analysis takes months and significantly lags financial reporting by 6-18months. At Emmi we have solved this headache for investors by quantifying and integrating climate analytics with the latest company financial disclosures.

If not using Emmi, you need a climate analytics provider that will allow you to report climate disclosures at the same time as your financial disclosures.

2. Financed emissions coverage

You need to quantify your financed emissions footprint - since the ISSB requires Scope 3 disclosure for investors.

There are huge data gaps in carbon, but don’t worry - at Emmi we use award-winning machine learning predictions to help you fill the carbon gap across all asset classes in days, not months. You can read more about our financed emissions module from a large Asset Owner case study here.

3. Scenario Analysis

ISSB mandates that companies conduct climate-related scenario analysis to evaluate their climate resilience.

See my previous newsletter here on how you can achieve this using the ASX300 as an example.

4. Transition Plan

ISSB requires companies to disclose details of their transition plans, such as critical assumptions and how they plan to resourcing activities outlined in the transition plan.

These plans must be specific enough to illustrate a company's overall strategy for transitioning to a lower-carbon economy, providing targets and actions for reducing greenhouse gas emissions.

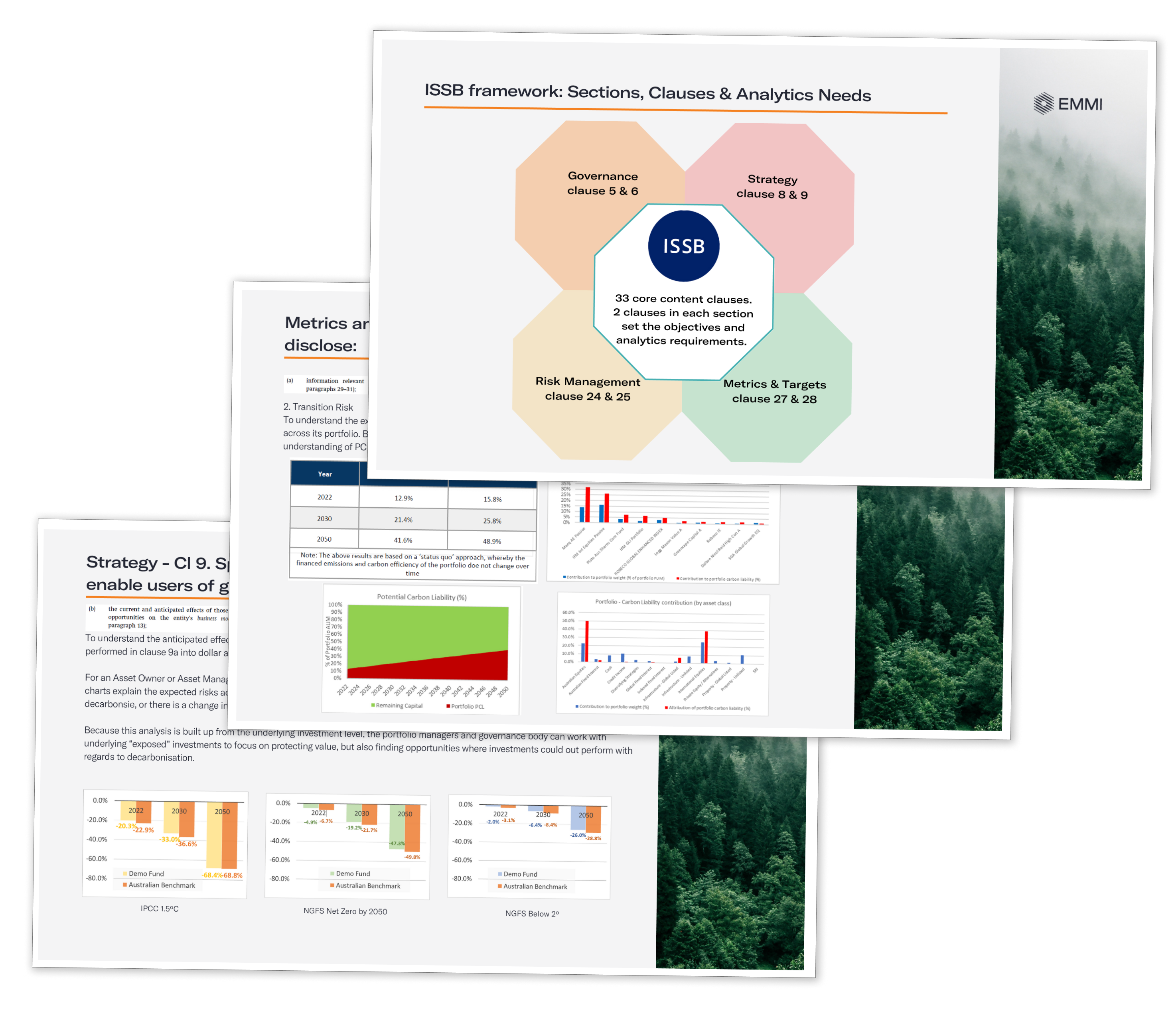

ISSB Reporting Template for Investors

The ISSB climate related disclosures require information on current climate exposures and how entities manage for future climate risks and opportunities. Some elements of IFRS S2 require qualitative descriptions of an entity’s process, but a large majority of IFRS S2 requires quantitative information like scenario analysis.

To help investors, we’ve gone through the IFRS S2 in detail pulling out the clauses where descriptive and quantitative analysis is needed and filling in the types of analysis you would need to report under ISSB. We provide a suggested structure that can be followed, explaining where entity specific narratives/qualitative information is needed.

You can sign up for our free ISSB template below and we'll walk you through everything you need.

Hope this helps and if you want to contact me you can just reply to this in your inbox..

Until next time.

Ben