Reported vs estimated emissions: what's better for investors?

Hello everyone,

There is a perception that corporate disclosures of carbon emissions are far more accurate than those that come from model estimates. Is there an accuracy-gap? For investors, this perception limits carbon integration into investment decision making and clouds our understanding of carbon exposure in markets.

So in this newsletter I want to explore how much emphasis we should place on data that is reported vs estimated. In reality, it’s a false choice. As I argue, both have limitations but are indispensable for investors in the foreseeable future. So rather than choose a side I provide perspective on how the next generation of carbon coverage can evolve using both.

What are ‘Reported’ Emissions?

Under the GHG protocol, companies measure and report carbon emissions using two methods: spend-based or activity-based. It’s very important to understand that reported emissions are also estimates and rely on emission intensity factors (which are also subject to large uncertainties).

Spend-Based Estimates

The spend-based method uses the value of goods and services purchased by an organization to estimate the amount released into the atmosphere. This method involves multiplying the organization's spending in an area (eg. fuel spend) by emissions intensity factors of the goods or services purchased (eg. CO2 per $ of fuel burnt).

Activity-Based Estimates

The activity-based method uses the units of the product or material to estimate the amount released into the atmosphere. So it involves quantifying the units or volume of a product used (eg tonnes of fuel) and using emission intensity factors (eg CO2 per tonne of fuel) to estimate the emissions associated with that activity.

Spend-based estimates are easier to use and get better coverage across a business while activity-based estimates are more accurate but impractical for most companies to use given the complexity of their products and supply chains. So in reality, the approach taken is mostly spend-based estimates with activity-based where they can.

Limitations of Reported Data for Investors

Accuracy

The biggest misnomer in the financial industry is the notion that reported data is very accurate. Even if reported emissions are audited, it’s very important to understand that:

Audits cover process not accuracy

The process for corporate carbon accounting has a significant potential uncertainty depending on the methods used, the data from millions of emission factors and the accuracy of categorising a product.

For many enterprises the errors in their reported emissions is significant. In 2021, a Boston Consulting survey of 1,290 executives found they estimate a 30-40% error in their reported carbon footprint calculations. In reality, errors will vary significantly depending on the company - unfortunately there is no systematic way to assess them across all companies.

Under-Reporting

Even if companies report emissions, they often don’t report the most complex and/or emissions intensive activities. We analysed all reported data between 2016 and 2021 for over 12,000 companies. For scope 3, companies often reported ‘Business Travel’ but didn’t report on far more intensive categories like ‘Use of Sold Products’. You can read more about that research here.

Portfolio Coverage is Small

Only 10% of the worlds public companies report emissions. For a typical multi-asset portfolio, listed equities and bonds make up about one-third of asset allocation. So relying only on reported data would typically cover less than 30% of a typical multi-asset portfolio.

Old Data

Typically, reported data is 12-18 months old.

What are ‘Estimated’ Emissions?

When a company doesn’t report emissions, what can analysts and investors do? Typically analysts and investors don’t have access to spending or activity-based data from within a company, so revenue is typically used.

Emission-Factor Estimates

Since public companies report their earnings to the market, spend-based methods can be used using revenue. This method involves multiplying the organization's revenue by emissions intensity factors revenue in similar companies. Emission factors are typically sourced using EEIO (Environmentally-Extended Input Output) models from organisations like the US EPA or the EU.

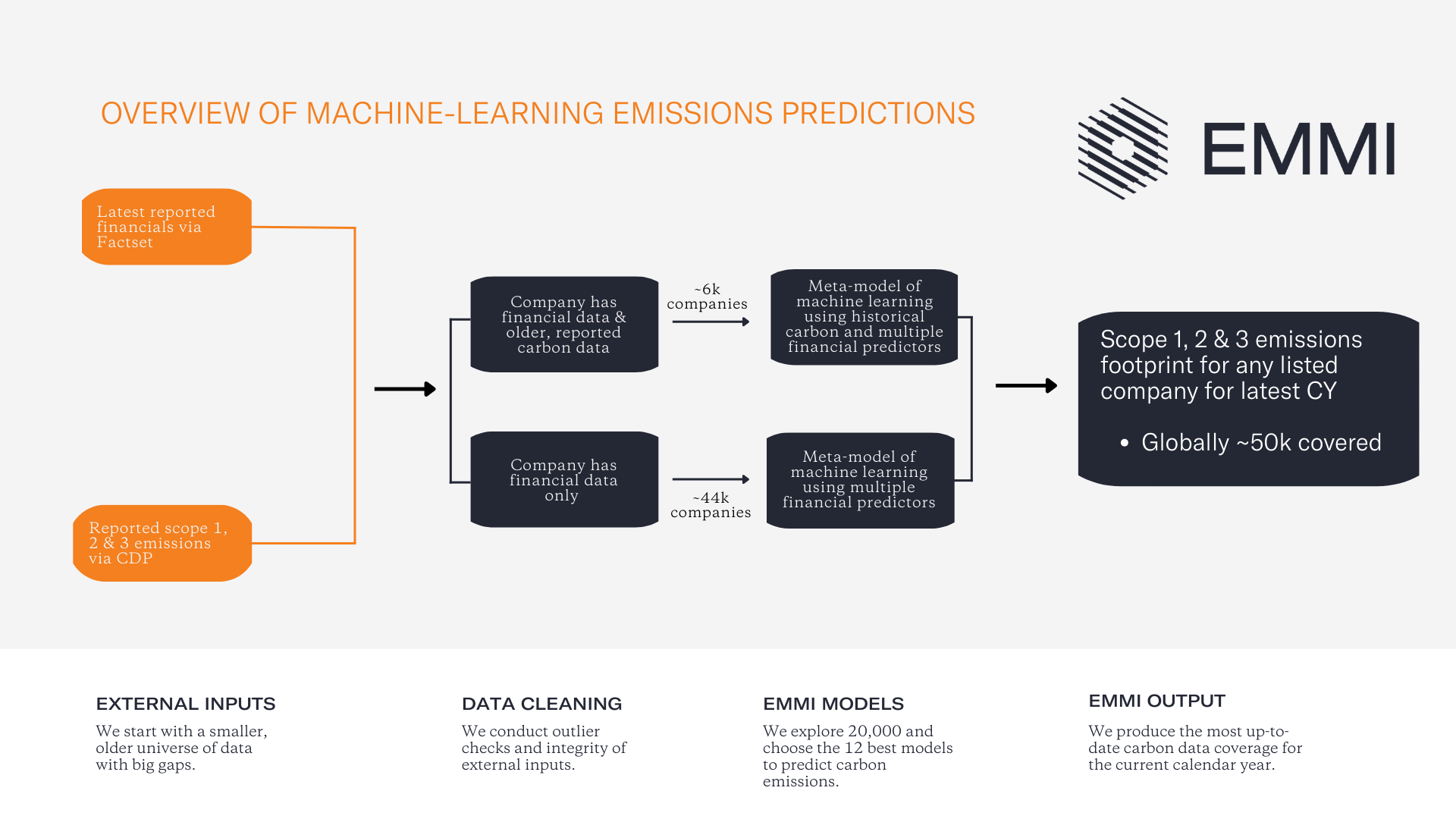

Machine-learning Estimates

A new approach that we have helped pioneer at Emmi is to use the reported data-set to train machine-learning models that predict emissions for any company from standard financial and business information. You can read more about this approach here. This approach doesn’t rely on static emission factors, but rather trains and adapts with the new reported data each year.

Limitations of Carbon Estimates for Investors

Accuracy

Relying on revenue and business information for a company is likely less accurate than spend or activity-based estimates. In reality, it’s hard to assess the difference in accuracy between reported and estimated. What we do know is that the machine-learning based approach is up to 30% more accurate than the simple revenue-based approaches.

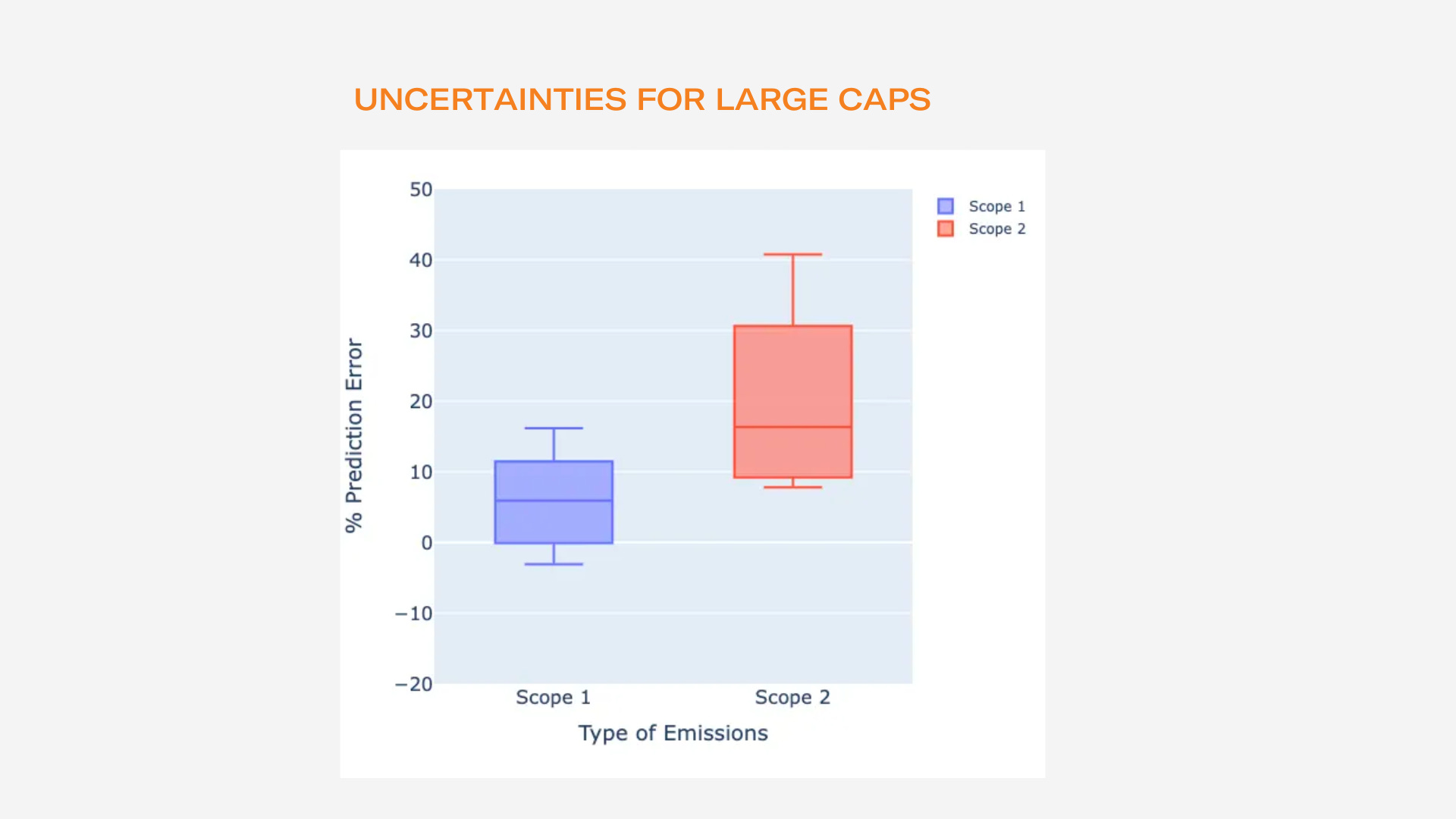

Overall for larger companies as an example, the accuracy of our machine-learning predictions are within 5-12% for Scope 1 and 15-30% for Scope 2 (see below). Interesting this is within the errors suggested by companies themselves in how they estimate reported emissions.

A better-hybrid approach for investors

For investors, there is no choice between reported and estimated emissions: you need to use both. For us at Emmi however, we use the reported numbers to build the next-generation of data prediction models in order to cover your portfolio.

Investors aren’t the government - so getting accuracy down to the last possible tonne of emissions per holding is not a priority. For investors, greater portfolio coverage and knowledge of the uncertainty allow for the best decisions to be made.

In reality, 20% of your portfolio will have a material exposure to carbon, and with new machine-learning estimates you now have a systematic way to check virtually all of your portfolio - then make decisions to go deeper or take actions when needed.

When reported emissions aren’t useful?

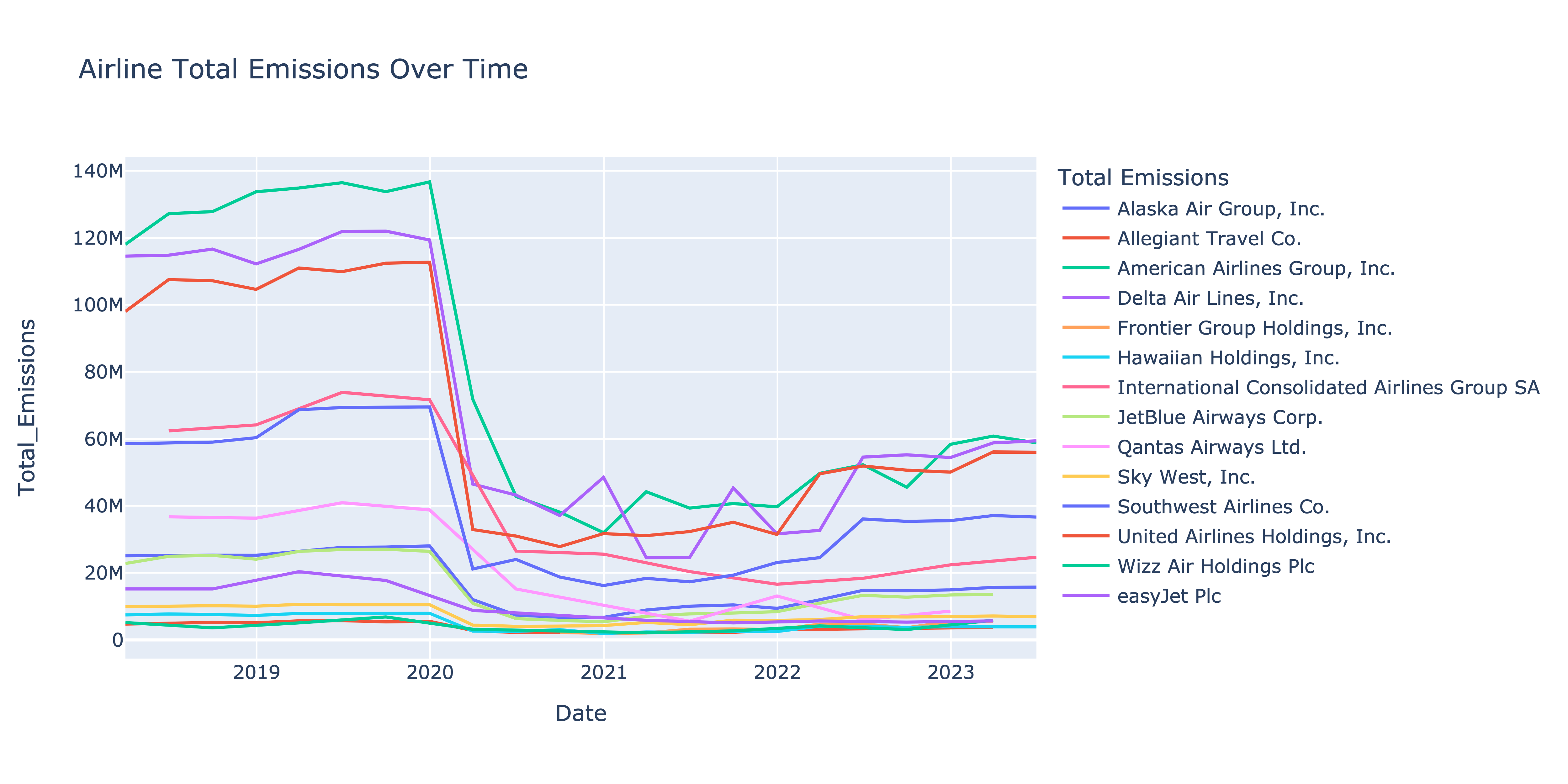

Take COVID-19 for example. The shutdown and financial collapse of airlines was immediate. Emissions fell off a cliff in a matter of months - but given reported emissions are typically 12-18months lagged - reported emissions were too old to be useful. On the other hand, our quarterly emission prediction models captured these timely drops well (see below).

Beyond better carbon information for investment decisions, greater coverage and timeliness of carbon data is important since carbon reporting standards like the ISSB are seeking carbon to be synchronised on a reporting schedule with finance. That isn’t possible with reported emissions and unlikely for many years.

But using the reported data-set as training for better machine-learning models is the only approach best equipped to allow for carbon disclosures to occur on a timescale relevant for finance/ISSB goals. Once reported emissions are eventually disclosed 12-18months after the fact, our models are recalibrated and learn from the new data - becoming even more accurate and useful for investors.

Given the uncertainties and complexities of reporting carbon across the market, reporting gaps in carbon are huge and will continue to be huge for many years. In the meantime, next-generation machine learning estimates use the growing reported data in order to fill the gaps and can do so within similar uncertainties than reported data. If you focus just on reported emissions, you miss a big opportunity to get better information to make investment decisions.

Thanks for reading. Until next time.

Ben